Chapter 4

Retail Market

Germany Real Estate Market Outlook 2024

Key Takeaways

- Framework conditions in an uptrend

Key factors of influence such as inflation and turnover indicate a favourable trend in stationary retail. - Demand running high on the leasing market

Strong demand characterizes the top locations and prime rents are in an uptrend, while the importance of secondary locations and small cities continues to dwindle. - Focus on large retail properties

A large number of shopping centers with a wide range of options will be offered on the retail investment market in 2024. Warehouse properties could also present interesting opportunities – due to operating companies once again running into difficulties. - Textile retail as a high performer

Trading in textiles, clothing, shoes and leather goods that have come under great pressure in recent years could prove to be the only segment to generate revenue in 2023, both in nominal and in real terms. - Yields showing the first signs of stabilizing

Following a steep increase in yields across all sub-asset classes of retail real estate, the first signs of stabilizing have been in evidence since the second half of 2023.

Uptrend in the general environment not yet tangible in the market

The economic challenges and exogenous shocks triggered by the war of aggression against Ukraine that sent inflation up by leaps and bounds continue to dominate the macroeconomic environment in Germany, with a direct impact on retail in the country.

- Consumers are still feeling the effects of price hikes, particularly with energy and food prices, even though the high inflation rate of up to 8.7% at the start of 2023 has meanwhile dropped over the course of the year to below 4% and current forecasts give rise to hope for a further slowdown as 2024 progresses in the direction of the 2% target. Nevertheless, the population’s real purchasing power contracted over the course of 2023. Not all products and goods were affected to the same extent by the price adjustments – only areas where exercising restraint was virtually impossible, leaving consumers with a choice of abstinence or shopping elsewhere. Other sectors where price rises were less pronounced were also impacted by consumer reticence, however.

- This situation is also reflected in consumer sentiment that remains subdued but nevertheless improved notably over the past year. Accordingly, the consumer climate index is still in negative territory, but brightened considerably over the year, from -37.6 points in January 2023 to -25.1 points in January 2024.

- Despite the general conditions outlined in the environment, retail in Germany was able to raise (nominal) sales again in 2023 even though a slight decline in real terms is to be anticipated from high inflation.

- The higher level of sales was particularly applicable to stationary retail that succeeded in winning back market shares from e-commerce. As a result, the exceptional boom experienced by e-commerce in the wake of the coronavirus pandemic is returning to its original trajectory.

- Stationary retail should also benefit from higher footfall that has finally shaken off the Covid-19 pandemic and prove impervious to the difficult economic environment.

Inasmuch, the general conditions for retail in Germany went one step further in returning to normal levels or even improved over the course of 2023, a development which has remained virtually unreflected on Germany’s retail market.

Prime rents on the retail leasing market rose slightly in 2023, for instance, and further marginal is anticipated in 2024. In this context, a more differentiated approach is necessary as an increasingly strong focus appears to be placed on hot spots in retail. Accordingly, a small number of cities and specific locations in them are considered highly desirable by retailers, while other, less favorable locations and also many C and D cities are struggling.

While luxury locations have developed particularly well, city center retail locations are generally in decline and less floor plate is required, particularly over and above the first floor.

The general reticence of investors remains evident in the retail investment market. Higher financing costs and the returns on alternative investments are curbing transaction activity and braking the customary momentum on the German retail real estate investment market. At €5.4 billion, the year 2023 delivered the lowest result since 2009 when, as a consequence of the financial crisis, just under €3.3 billion was allocated on Germany’s retail investment market.

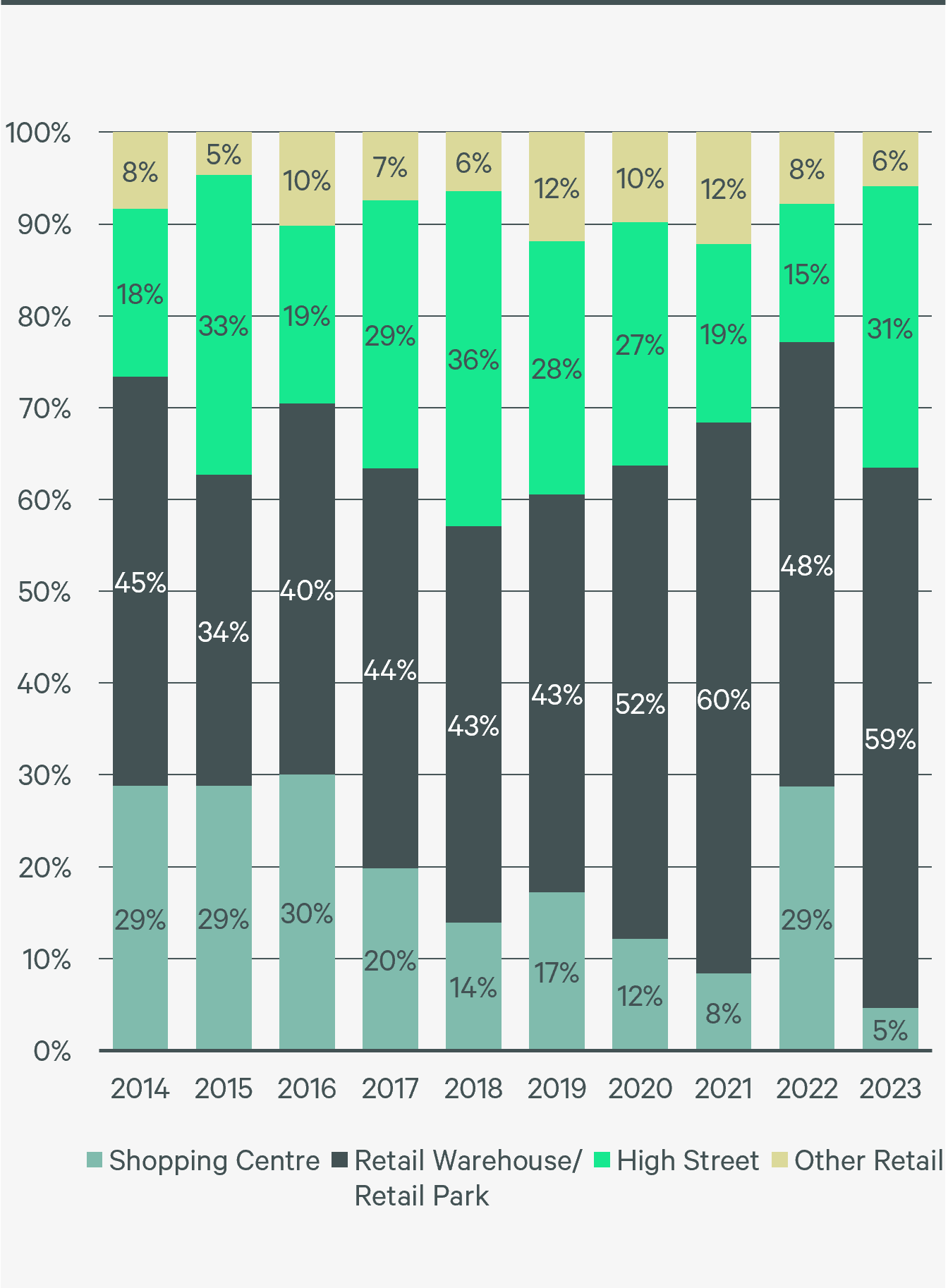

Retail warehouse properties dominated market activity in 2023, having already succeeded in steadily expanding their share in previous years. At present, these properties are deriving additional benefit from the current financing conditions. While large-scale transactions, whose financing presents a very special challenge in the current market environment, have virtually come to a standstill, investors are favouring transactions in a volumes between €10 million and €40 million. With their typical deal size, retail warehouse properties ideally suit investors’ criteria and will continue to be in demand in 2024, particularly as a trend towards yields stabilizing is materializing in this segment. Fire sales are not expected here.

2024 – The Year of the Shopping Center?!

Conversely, shopping centers played virtually no role at all on Germany’s retail investment market. Given the more complex financing, the gap between price expectations of buyers and sellers, and skepticism regarding the future viability of the shopping center concept, hardly any centers had changed hands at the last count. Much brisker transaction activity is expected here as from 2024. At the present point in time, around one in five of the 328 shopping centers defined by CBRE in Germany may possibly be offered for sale. Analyzing these properties reveals that these centers are generally not distressed assets requiring commensurate action and additional financing, but instead make the core or core plus grade.

Transaction volume by use type

Source: CBRE Research

Furthermore, these centers potentially coming up for sale offer a good mix of various location-related classes. Classes include, on the one hand, large-scale locations in cities of various categories, from the major cities through to regional centers and on to prosperous B locations. On the other hand, small-scale locations embedded in the local municipality, with both inner-city centers, properties in various districts and centers on "greenfield sites" also feature.

The investment potential here is demonstrated by taking the average purchase price of shopping centers of the last five years as a basis, which results in a potential investment volume of between €5 and €6 billion. Even if a transaction naturally depends on other factors, this sales pipeline forms a good initial basis for a sound performance in this sub-asset class, especially as opportunities are available for different investors and investment strategies.