Chapter 8

Healthcare & Later Living

Germany Real Estate Market Outlook 2024

Key Takeaways

- Later living and Healthcare Real Estate

Germany is ageing. The need for forms of living and care appropriate for older people is rising in tandem with steady growth in the proportion of older people in the overall population. - Care homes and assisted living dominate the investment market

Healthcare facilities continue to dominate Germany’s investment market. Given the less stringent regulatory requirements, investors are nevertheless increasingly devoting their attention to assisted forms of living and service living for senior citizens. - Operator insolvencies and political imponderables as the greatest risks

A slew of operator insolvencies resulting from cost increases, and nursing care insurance funds failing to adjust refinancing options caused investors to hold back. Clear, nationwide, standardized political guidelines for setting up and operating care facilities will generate more confidence for the necessary investment. - Growing investor appetite for outpatient healthcare properties

Growing emphasis on outpatient treatment in providing healthcare is eliciting the interest of investors in contemporary, efficient healthcare properties such as medical centers and medical service centers. - Private capital urgently needed – appeal to the policymakers

Private capital wanting to generate sufficient return is urgently needed for the development and expansion of a modern social infrastructure revolving around medical and care facilities. Policymakers are called upon to create the framework conditions conducive to investors.

Private capital urgently needed for transforming the social infrastructure

Higher risks, higher returns

Investor appetite for alternative real estate asset classes has been growing for a number of years. The focus of professional investors has been placed above all on healthcare property and real estate for later living. Two factors are decisive here: the easily forecastable fundamentals of this real estate in an ageing society, along with the relative imperviousness to economic fluctuations ascribed to asset class of healthcare. Since the outbreak of the coronavirus pandemic, institutional investors above all are showing a stronger interest in using these alternatives for reason of their higher yields to diversify their existing portfolios, or also for the purpose of launching their own asset-class specific vehicles. Thanks to the associated social aspects (Impacts), this is also instrumental in achieving targeted ESG objectives.

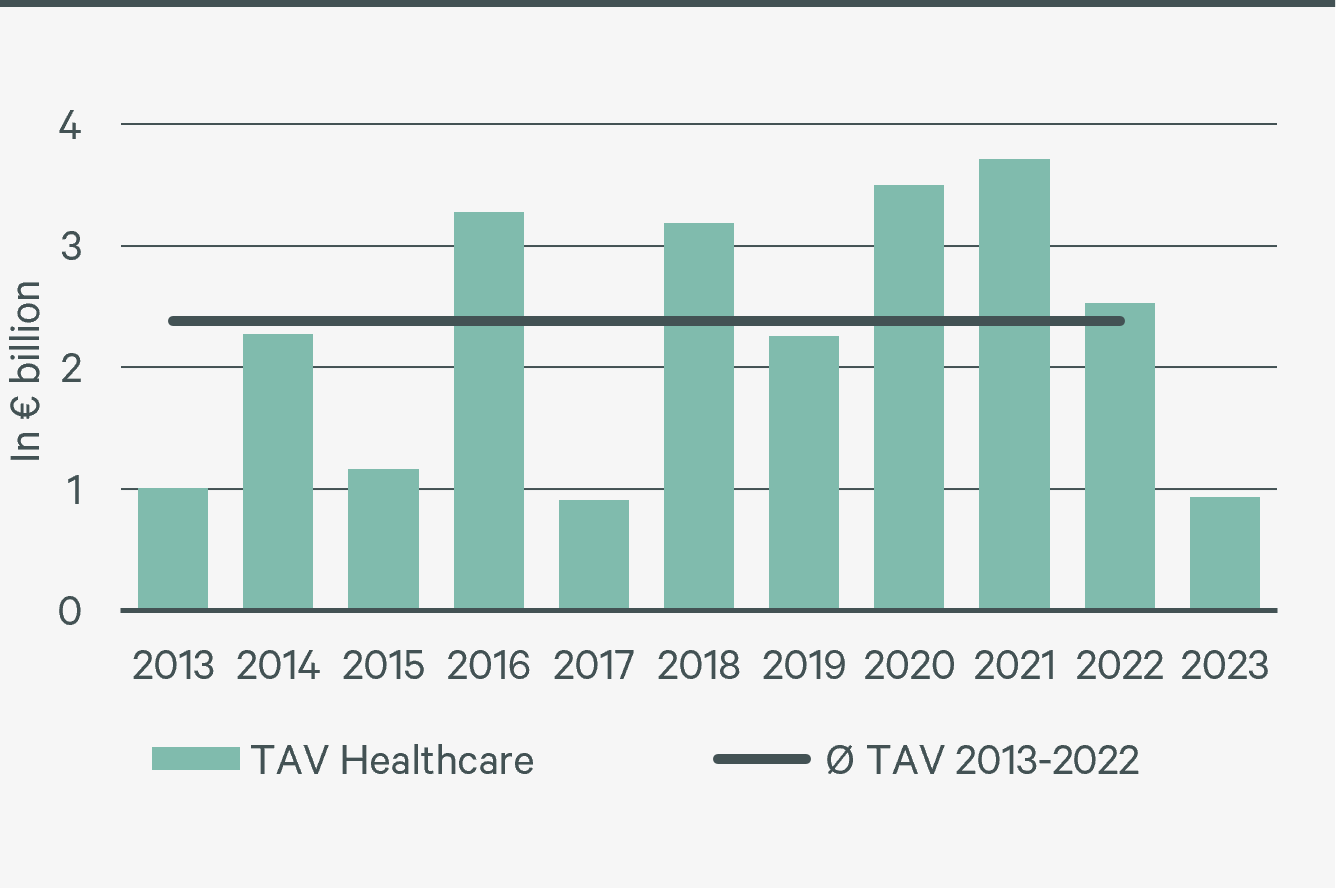

As in years gone by, 2023 produced renewed proof that the transaction volume on the German healthcare real estate investment market depends on large-scale transactions. If these deals fail to materialize, investment activity remains modest. In the year now ended, no transactions in the triple-digit million range were registered. The sharp increase in financing costs, compounded by the limited willingness of banks to accompany large-scale transactions, put the brakes on momentum in the investment market. As a result, the portfolio share came in at 30%, marking the lowest point since 2009. The situation was exacerbated by the general reticence of market players due to differing price expectations and the cherry-picking approach of investors when investing in care homes, to which a number of operator insolvencies also contributed.

Healthcare transaction volume – Germany

Source: CBRE Research

Healthcare investments by asset class

Source: CBRE Research

Investment opportunities alongside conventional care

The overall transaction volume in 2023 fell just short of the one-billion-euro mark, thus approximating the level of 2017. The proportion of international investors came in at 17%, down 29%-points compared with 2022. All in all, the share of the entire transaction volume registered in Germany therefore stood at 3.2%, which roughly corresponds to the long-term average since 2009.

The steepest decline was sustained by medical centers and medical service centers. At €39 million, the transaction volume plunged 93% compared with the year-earlier result that nevertheless set a new record at around €541 million. Here it becomes evident that the supply of contemporary and high quality outpatient healthcare properties in the market is in no way able to cater to huge investor demand.

Although not reflected in the 2023 investment volume, huge interest in properties beyond the boundaries of inpatient care is observable. Medical centers, for instance, have caught the interest of many investors who were formerly more active in other commercial real estate classes. (Excessive) regulation by the policymakers and the associated operator risk, as exists in in patient care, is manageable for medical centers and medical service centers. At the same time, more product in the field of inpatient care establishments and systemically relevant real estate such as rehab clinics and clinics in general is likely to come on the market in the future due to consolidation on the operator market and the hospital reform planned for 2024. There are, for instance, operator investors who opt for sale-and-leaseback for properties acquired together with the operators.

Investor appetite for alternative real estate asset classes has been growing for a number of years. The focus of professional investors has been placed above all on healthcare property and real estate for later living. Two factors are decisive here: the easily forecastable fundamentals of this real estate in an ageing society, along with the relative imperviousness to economic fluctuations ascribed to asset class of healthcare. Since the outbreak of the coronavirus pandemic, institutional investors above all are showing a stronger interest in using these alternatives for reason of their higher yields to diversify their existing portfolios, or also for the purpose of launching their own asset-class specific vehicles. Thanks to the associated social aspects (Impacts), this is also instrumental in achieving targeted ESG objectives.

As in years gone by, 2023 produced renewed proof that the transaction volume on the German healthcare real estate investment market depends on large-scale transactions. If these deals fail to materialize, investment activity remains modest. In the year now ended, no transactions in the triple-digit million range were registered. The sharp increase in financing costs, compounded by the limited willingness of banks to accompany large-scale transactions, put the brakes on momentum in the investment market. As a result, the portfolio share came in at 30%, marking the lowest point since 2009. The situation was exacerbated by the general reticence of market players due to differing price expectations and the cherry-picking approach of investors when investing in care homes, to which a number of operator insolvencies also contributed.

Healthcare transaction volume – Germany

Source: CBRE Research

Healthcare investments by asset class

Source: CBRE Research

Investment opportunities alongside conventional care

The overall transaction volume in 2023 fell just short of the one-billion-euro mark, thus approximating the level of 2017. The proportion of international investors came in at 17%, down 29%-points compared with 2022. All in all, the share of the entire transaction volume registered in Germany therefore stood at 3.2%, which roughly corresponds to the long-term average since 2009.

The steepest decline was sustained by medical centers and medical service centers. At €39 million, the transaction volume plunged 93% compared with the year-earlier result that nevertheless set a new record at around €541 million. Here it becomes evident that the supply of contemporary and high quality outpatient healthcare properties in the market is in no way able to cater to huge investor demand.

Although not reflected in the 2023 investment volume, huge interest in properties beyond the boundaries of inpatient care is observable. Medical centers, for instance, have caught the interest of many investors who were formerly more active in other commercial real estate classes. (Excessive) regulation by the policymakers and the associated operator risk, as exists in in patient care, is manageable for medical centers and medical service centers. At the same time, more product in the field of inpatient care establishments and systemically relevant real estate such as rehab clinics and clinics in general is likely to come on the market in the future due to consolidation on the operator market and the hospital reform planned for 2024. There are, for instance, operator investors who opt for sale-and-leaseback for properties acquired together with the operators.