Chapter 7

Hotel

Germany Real Estate Market Outlook 2024

Key Takeaways

- Stabilization of hotel markets

Over the past year, the hotel markets staged a significant recovery, boosted in particular by the good development of rates. Major events such as the European Football Championship and growth in business and trade fair tourism can be expected to positively impact the rebound in performance in the coming year, now driven above all by rising occupancy. By contrast, rate increases similar to the year now ended are in all probability unlikely to be implementable. - Cost pressure and staff shortages remain critical

While hotel operators have already experienced a sharp increase in costs in recent years, this will remain an important factor in the coming year as well. Along with partly sharp increase rents on the back of index adjustments, rising personnel costs above all, as well as the retraction of the VAT concession, will squeeze margins. - Strong competition for hotel development

The market’s upbeat recovery has caused hotel operators to refocus on expansion. A countervailing force emanates from the lack of supply due to the decline in new developments. - Existing stock in high demand

Only 14% of the transaction volume in 2023 was attributable to core transactions and more than 90% of the transaction volume consisted of existing properties. Two types of properties are currently in high demand: core properties with long-term leases where the price discovery process has not yet been fully completed, and properties with no operators and upside potential. - Growing interest in hotel properties

The hotel transaction market closed the year 2023 with the strongest quarter since the start of 2020, which is evidence of the growing interest in hotel real estate. This trend is expected to hold steady in the coming year as well, thus contributing to the investment market’s steady recovery.

Interest in hotel asset class on the rise

The hotel market delivers proof of its resilience despite the challenges

Overnight figures are impressive proof that demand has found its way back to the growth path. The figures collated by the German Statistical Federal Office through to November inspire confidence. Up until this point in time, accommodation establishments in Germany recorded 457 million overnight stays of domestic and foreign guests, reflecting an increase of 8% compared with the year-earlier period.

A series of imminent major events, first and foremost the European Football Championship in the summer, will boost the number of overnight stays in 2024. In addition, business and group travel is signalling further recovery even though many companies are having to deal with budget constraints. In the long term, a growing shift toward “consumer experience” is detectable – another positive impact on the demand for hotel accommodation.

Hotel operators will nevertheless have to face major challenges. The sharp increase in operating costs at the last count will particularly impact the profitability of some hotels. Against this backdrop, more cost-effective hotel concepts and the luxury hotel business that is in a position to compensate for rising costs through higher prices are proving particularly resilient.

Source: Destatis, CBRE Research

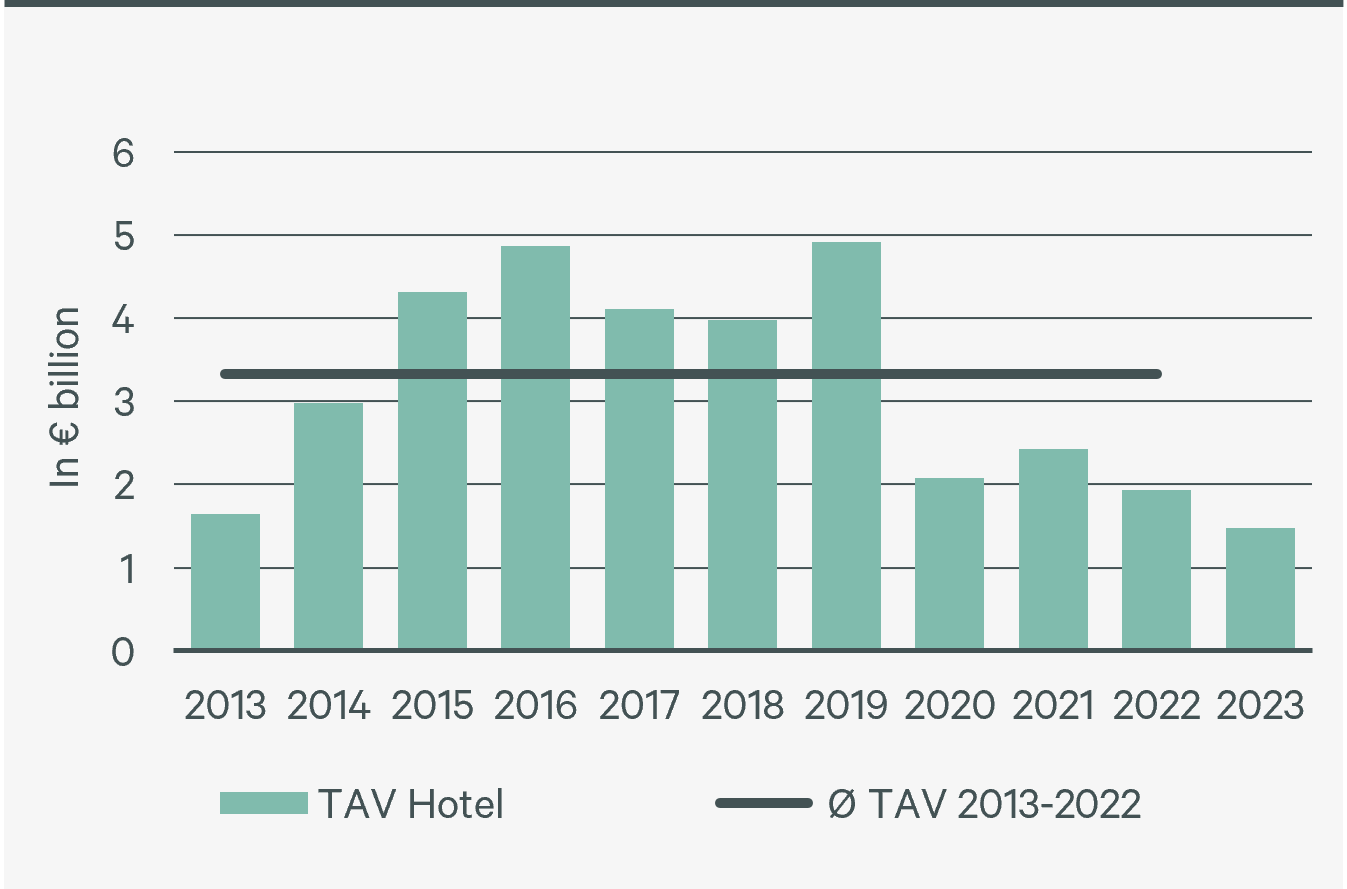

Hotel transaction volume – Germany

Source: CBRE Research

Cautious optimism – uptrend on the German hotel investment market

After the slump caused by the pandemic, Germany’s hotel markets have recovered more swiftly than expected. This dynamic trend has caught the interest of investors and currently offers attractive opportunities for them to position themselves on the German real estate market and benefit from the hotel market’s positive performance.

The hotel investment market achieved transaction volume of €1.47 billion in 2023. Although this is the lowest volume since 2012, corresponding to a decline of 24 percent year on year, the decrease in the transaction volume was also the lowest of all the asset classes.

The repricing process is also progressing. While, at the end of 2022, gross initial yields of 4.65% were still achievable for hotel properties leased long term in the Top 5 cities, the prime yield rose by 60 basis points in total to 5.25% over the course of 2023. In this scenario, demand is especially on the rise for existing properties, either with well secured and long-term lease agreements or with no operators, and thus with value-add potential. Properties of this kind attracted more than 90% of the volume in 2023.

The positive market development, combined with interest rates stabilizing, gives rise to expectations in 2024 for more activity on the hotel transaction market, ultimately also for reason of the greater challenges facing other asset classes, meaning that investors are on the lookout for portfolio diversification.