Chapter 9

Life Sciences

Germany Real Estate Market Outlook 2024

Key Takeaways

- Dynamic cluster

Along with academic educational institutions and hospitals, companies from the field of life science function as an anchor in facilitating the creation of a dynamic ecosystem of scientific disciplines. - Rising rent levels

Life science companies prefer to lease space that is well equipped and, with the competition for highly qualified employees in mind, are moving closer to the center of office market. - Fully equipped laboratories

While the majority of laboratory space is used by owner-occupiers, start-ups have the possibility of leasing operator-run, fully equipped laboratory space and of benefiting from spillover effects. - Venture capital challenges

The difficult financing environment is forcing investors to be more selective in allocating capital. Maturing start-ups appeal to investors as success can be generated more rapidly here. - Crisis-resilient asset class

The secure, stable cash flow from long-term anchor tenants and momentum in the start-up scene may enable the life science sector to evolve from a niche category into an asset class in its own right on Germany’s real estate market.

Dynamic cluster formation and rising requirements placed on location and fit-out characterize the life science sector.

Focus of German life science companies

The life science sector is a complex ecosystem of interconnected industries encompassing manifold knowledge-intensive and often highly specialized companies. This includes companies in the field of biotechnology/informatics, pharmaceuticals, medical technology, digital health, consultancy firms, as well as state-owned and non-profit organizations participating in the various phases of research, development, technology transfer, along with sales and distribution. The life science sector in Germany currently comprises more than 4,000 enterprises, with interdisciplinary biotech companies accounting for the largest share. In 2023, these companies also focused on the development of oncology compounds in the form of antibodies or immune therapies. Medical technology is expanding its share in the overall market, with activities focused primarily on the use of technical equipment.

Life science clusters frequently locate close to academic institutions or hospitals, such as the University Hospital of Heidelberg or Ludwig-Maximilian University in Munich. Large companies can also assume an anchor function for the formation of clusters and enable a dynamic ecosystem of scientific disciplines. One example is the pharmaceutical company Pfizer that has already established hubs like these in Freiburg and Berlin. The most renowned clusters are located in the aforementioned cities and will continue to expand in 2024, fostered by a fundamentally positive environmental conditions in Germany as a production location, in the surrounding Rhine-Neckar region, Stuttgart, the Frankfurt/Rhine-Main region, Cologne and Hamburg.

Share of companies by sector

Source: German Biotech Database, CBRE Research

Source: German Biotech Database, CBRE Research

Top 5 leasing, take-up and rents

Source: CBRE Research

Leasing market

In contrast to traditional office occupiers, life science companies mainly lease laboratory space with the requisite office space. The requirements placed on premises tend to vary quite considerably as the focus of activity may be very different. Owing to the many established companies, a large proportion of life science properties are occupied by their owners. The supply on the leasing market is therefore limited. A look at the take-up of office space in the research, pharmaceutical and biotech sectors in the Top 5 German markets nevertheless offers starting point for analyzing demand. With a take-up volume averaging 85,000 sq m, the sector displays stable demand but, similar to the market as a whole, recorded a decline in take-up in 2023. A look at rental development reveals a rental price level in the sector that has been below the average for years. In the past five years, the sector has nevertheless registered rental growth of 39% and, in the last three years, has therefore exceeded the general average rent. The competition for highly qualified employees is forcing companies to relocate away from bland industrial zones to central, attractive locations.

Whereas major, established companies also take laboratory space in superior-finish shell or only partially equipped, start- and scale-ups opt for modular and flexible units that are already fully equipped. The most recent example is the Skygate Biotech hub in Munich that, along with fully equipped laboratories, also offers new work office space for better collaboration. This trend is set to persist in 2024 as well.

The life science sector is a complex ecosystem of interconnected industries encompassing manifold knowledge-intensive and often highly specialized companies. This includes companies in the field of biotechnology/informatics, pharmaceuticals, medical technology, digital health, consultancy firms, as well as state-owned and non-profit organizations participating in the various phases of research, development, technology transfer, along with sales and distribution. The life science sector in Germany currently comprises more than 4,000 enterprises, with interdisciplinary biotech companies accounting for the largest share. In 2023, these companies also focused on the development of oncology compounds in the form of antibodies or immune therapies. Medical technology is expanding its share in the overall market, with activities focused primarily on the use of technical equipment.

Life science clusters frequently locate close to academic institutions or hospitals, such as the University Hospital of Heidelberg or Ludwig-Maximilian University in Munich. Large companies can also assume an anchor function for the formation of clusters and enable a dynamic ecosystem of scientific disciplines. One example is the pharmaceutical company Pfizer that has already established hubs like these in Freiburg and Berlin. The most renowned clusters are located in the aforementioned cities and will continue to expand in 2024, fostered by a fundamentally positive environmental conditions in Germany as a production location, in the surrounding Rhine-Neckar region, Stuttgart, the Frankfurt/Rhine-Main region, Cologne and Hamburg.

Share of companies by sector

Source: German Biotech Database, CBRE ResearchTop 5 leasing, take-up and rents

Source: CBRE Research

Leasing market

In contrast to traditional office occupiers, life science companies mainly lease laboratory space with the requisite office space. The requirements placed on premises tend to vary quite considerably as the focus of activity may be very different. Owing to the many established companies, a large proportion of life science properties are occupied by their owners. The supply on the leasing market is therefore limited. A look at the take-up of office space in the research, pharmaceutical and biotech sectors in the Top 5 German markets nevertheless offers starting point for analyzing demand. With a take-up volume averaging 85,000 sq m, the sector displays stable demand but, similar to the market as a whole, recorded a decline in take-up in 2023. A look at rental development reveals a rental price level in the sector that has been below the average for years. In the past five years, the sector has nevertheless registered rental growth of 39% and, in the last three years, has therefore exceeded the general average rent. The competition for highly qualified employees is forcing companies to relocate away from bland industrial zones to central, attractive locations.

Whereas major, established companies also take laboratory space in superior-finish shell or only partially equipped, start- and scale-ups opt for modular and flexible units that are already fully equipped. The most recent example is the Skygate Biotech hub in Munich that, along with fully equipped laboratories, also offers new work office space for better collaboration. This trend is set to persist in 2024 as well.

Growth in venture capital is mirrored by the demand for laboratory space.

Financing challenges and solutions

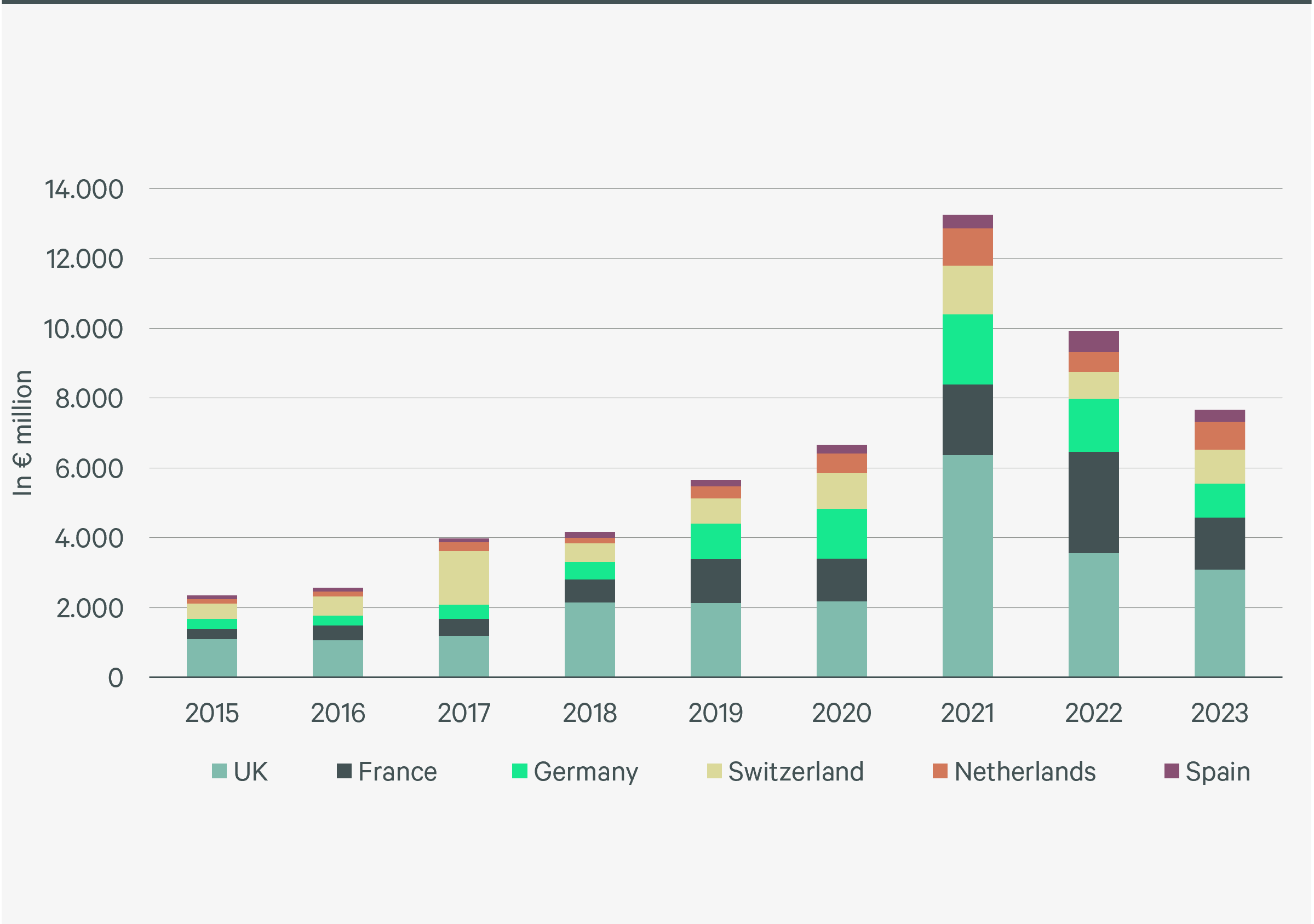

Similar to many other sectors, the life science industry struggled in the past year with higher interest rates, weaker economic strength and geopolitical challenges. The numerous start-ups and scale-ups that largely define the sector depend to a great extent on financing through venture capital. Especially in the initial phase, research and development requires a great deal of capital, and achieving success that generates a profit may involve an indefinite period of time. The boom phase of biotech companies in the pandemic years of 2020 and 2021 was followed by a decline in venture capital activity that returned to pre-coronavirus level in Germany in 2023. The volume of borrowing in the country came in at just under one billion euros in the year now ended. In this difficult financing environment, companies at an advanced research stage garner investor attention as success can be more rapidly achieved here. In a European comparison, Germany is still in its infancy regarding its development in the field of life science and, in terms of capital venture financing volumes, ranks behind the United Kingdom and France.

The sale-and-leaseback transaction on Berlin’s investment market in the peripheral areas demonstrated one possibility of freeing up capital. Biotech company Scienion sold the new extension in the Adlershof Technology Park to investor BEOS and secured a 15-year lease agreement for itself, which enabled it to concentrate investments on its core business again. With a factor of 15.8, the transaction therefore approached the level of a prime yield of 6.7% for office property in the periphery of Berlin.

Life science real estate is generally proven to be less crisis prone and offers a steady cash flow based on anchor tenants with long-term leases. Once the financing environment stabilizes, venture capital will start to flow again into start-ups in the seed phase, which will boost the demand for laboratory space.

Venture Capital Life Sciences – domestic comparison (in € million)

Source: Dealroom, CBRE Research

Similar to many other sectors, the life science industry struggled in the past year with higher interest rates, weaker economic strength and geopolitical challenges. The numerous start-ups and scale-ups that largely define the sector depend to a great extent on financing through venture capital. Especially in the initial phase, research and development requires a great deal of capital, and achieving success that generates a profit may involve an indefinite period of time. The boom phase of biotech companies in the pandemic years of 2020 and 2021 was followed by a decline in venture capital activity that returned to pre-coronavirus level in Germany in 2023. The volume of borrowing in the country came in at just under one billion euros in the year now ended. In this difficult financing environment, companies at an advanced research stage garner investor attention as success can be more rapidly achieved here. In a European comparison, Germany is still in its infancy regarding its development in the field of life science and, in terms of capital venture financing volumes, ranks behind the United Kingdom and France.

The sale-and-leaseback transaction on Berlin’s investment market in the peripheral areas demonstrated one possibility of freeing up capital. Biotech company Scienion sold the new extension in the Adlershof Technology Park to investor BEOS and secured a 15-year lease agreement for itself, which enabled it to concentrate investments on its core business again. With a factor of 15.8, the transaction therefore approached the level of a prime yield of 6.7% for office property in the periphery of Berlin.

Life science real estate is generally proven to be less crisis prone and offers a steady cash flow based on anchor tenants with long-term leases. Once the financing environment stabilizes, venture capital will start to flow again into start-ups in the seed phase, which will boost the demand for laboratory space.

Venture Capital Life Sciences – domestic comparison (in € million)

Source: Dealroom, CBRE Research