Chapter 5

Logistics Market

Germany Real Estate Market Outlook 2024

Key Takeaways

- Marginal decline in the construction project pipeline

The logistics market is not showing any signs of a developer crisis as can be observed in many other real estate segments. However, the construction project pipeline is contracting or slowing due to sluggish occupier demand, a shortage of suitable land and higher construction and financing costs. - Only moderate increase in vacancies

The vacancy rates will initially rise only moderately in 2024, while remaining at a low level far short of the historical average, also in an international comparison. Once the market recovers, which is expected in the second half of 2024, vacancy rates should stabilize.

-

Rental price trends – stay versus go

Sound rental price growth is an argument in favor of this asset class but may act as a barrier preventing tenants from moving, while increasingly resulting in rental agreements renewals rather than new leases being signed. -

Differentiation ongoing

Differences in the assessment of properties in terms of location, quality and price are likely to become more pronounced and the price gap regarding rent and purchase prices to widen further. -

Demand expected to remain sound

A moderately upbeat trend can be anticipated on the industrial and logistics market, in terms of occupiers as well as investors.

Lackluster momentum on the German industrial and logistics real estate market – slight contraction in the construction pipeline

After two consecutive years producing record results on Germany’s industrial and logistics property market, 2023 saw take-up of 5.35 million sq m, reflecting a decline of around 35% measured against the very good year-earlier result (8.21 million sq m). Comparison with the long-standing average of the last ten years also shows a result that has fallen by around 20%. The marked decline in 2023 take-up is attributable to several demand- and supply-side reasons.

A key factor consists of slowing demand in retail and most particularly in e-commerce. The boom in online trading caused by the pandemic that fueled exceptional growth in requirements for logistics space and triggered rapid capacity expansion in this segment is over and done with. According to current forecasts, e-commerce sales are therefore likely to have stagnated in 2023 or even dipped a little, both in real and in nominal terms. Consequently, very few inquiries for new space came from e-tailers. In many cases, space that could not be used by the actual tenants engaging in e-commerce was even sublet. Although online trading will continue to expand in the future and require logistics space, it will nevertheless return to its original development pathway with growth expected in the region of “only” one percentage point a year.

Furthermore, sustained economic uncertainty is dragging on the traditional logistics sector’s drive toward expansion. Although the outlook for the first six months of 2024 remains modest, momentum is likely to accelerate as from mid-year and particularly in the year thereafter, and with it also the demand for industrial and logistics premises. Furthermore, endeavors aimed at outsourcing and restructuring supply chains underway since the pandemic, including nearshoring strategies, have been stepped up in the face of the latent Taiwan conflict and the Houthi rebels attacks on ships passing through the Red Sea. This will give rise to increased requirements for space.

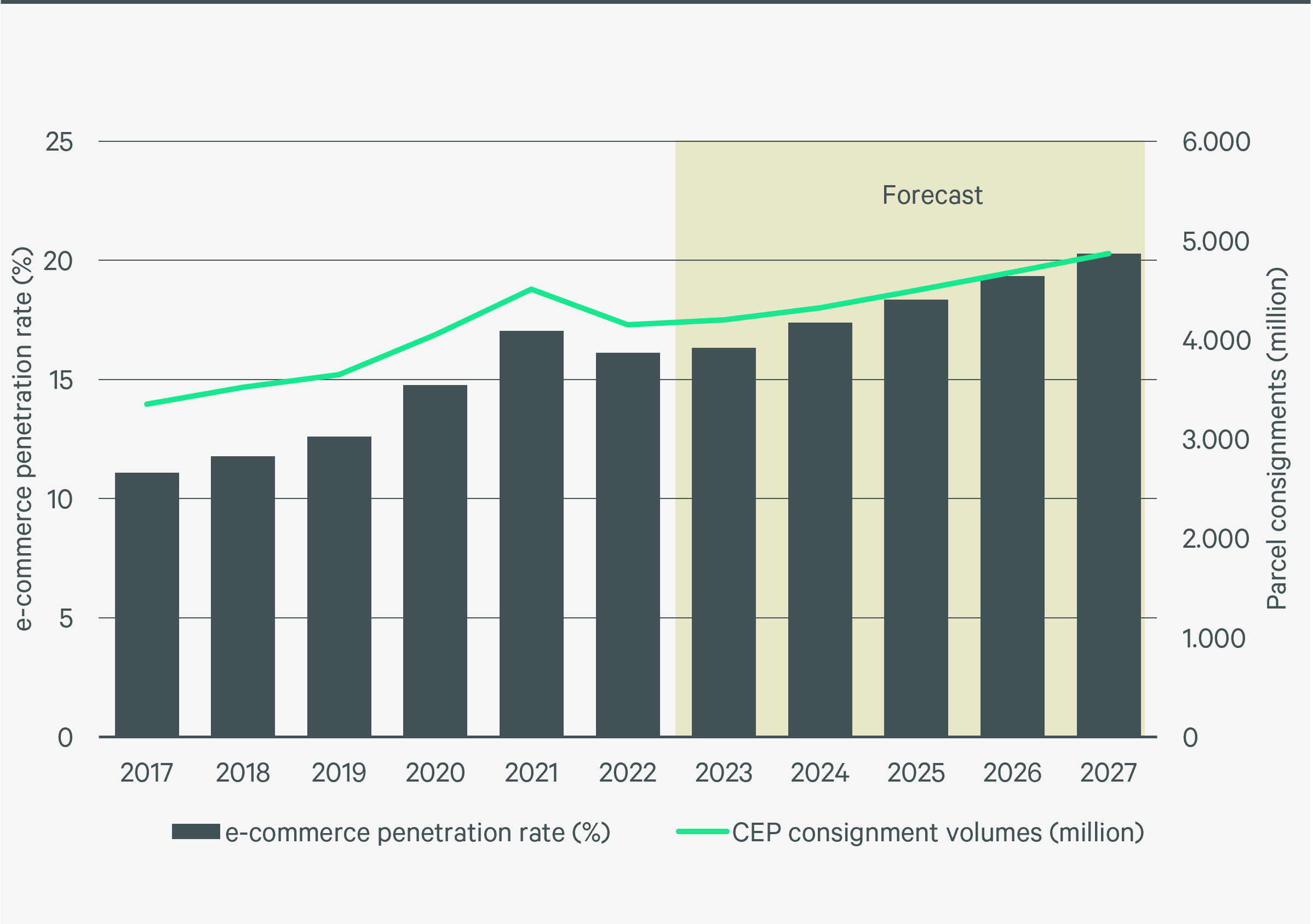

Development of e-commerce in Germany, including forecast

Source: KEP Study 2023 (Bundesverband Paket und Expresslogistik (BIEK), CBRE Research

Growing differentiation expected in the market

Ultimately, the sharp increases in rent will elicit more caution from companies that will tend toward renewing leases rather than relocating. Rental renewals that are generally cheaper for tenants than moving to new premises are not recorded as take-up.

However, these lease extensions also mean that, despite the lower take-up, the vacancy rate has only risen slightly and is still hugging a very low level. Although vacancies are likely to increase again moderately, they will continue to fall significantly below the historical averages.

This development is also explained by the fact that developers have reduced their development pipeline in the face of lower occupier demand and financing conditions made difficult by rising key rates and banks adopting a more cautious stance. Toward the end of 2022, the new-build pipeline for industrial and logistics real estate under construction dropped 13% to 3.5 million sq m. Rents and yields have nevertheless now reached a level that makes building a logistics property economically viable again. Furthermore, the demand for contemporary properties is steadily trending up, while follow-on rentals for older stock are becoming increasingly problematic, particularly if buildings do not fulfil ESG requirements.

Over the course of 2023, the prime rent for logistics properties rose sharply by 13% across the Top 5 markets, signifying substantial real growth despite high inflation.

Source: CBRE Research

Investment volume for logistics real estate and share in commercial transaction volume

Source: CBRE Research

Space was nevertheless lacking in 2023 as well, particularly in the highly desirable locations, which pushed prices up. Many rents for existing buildings, often based on leases with rent indexation, have also increased considerably on the back of inflation running at 5.1%. In 2024, we assume that the above-average uptrend in rental prices will slow, and that prime rents will rise in line with the inflation rate.

Occupier demand for contemporary space that is partly only insufficient and cannot be covered on an ad-hoc basis, the very moderate vacancy levels, along with attractive rental price growth have ensured strong investor interest in logistics properties, particularly as this asset class has delivered proof of its relevance for society and the economy.

As a result, logistics real estate advanced to take its place as the largest segment on Germany’s real estate investment market in 2023, with a transaction volume of €6.95 billion. The market benefited from an only marginal gap in buyer and seller price expectations and proved to be comparatively robust at the end of the year as well – even though, despite easing financing conditions, yields rose once again to 4.3% owing to various macroeconomic factors of uncertainty.

In 2024, we anticipate that both occupier and investor demand will hold steady. The market will continue to present a disparate picture, with the price gap between new, premium units and older, second hand buildings.